Najib and son fail to get Federal Court to hear constitutional issues on tax appeals

Judge says the court prefers to proceed with the appeal proper which would cover the constitutional issues as well as others.

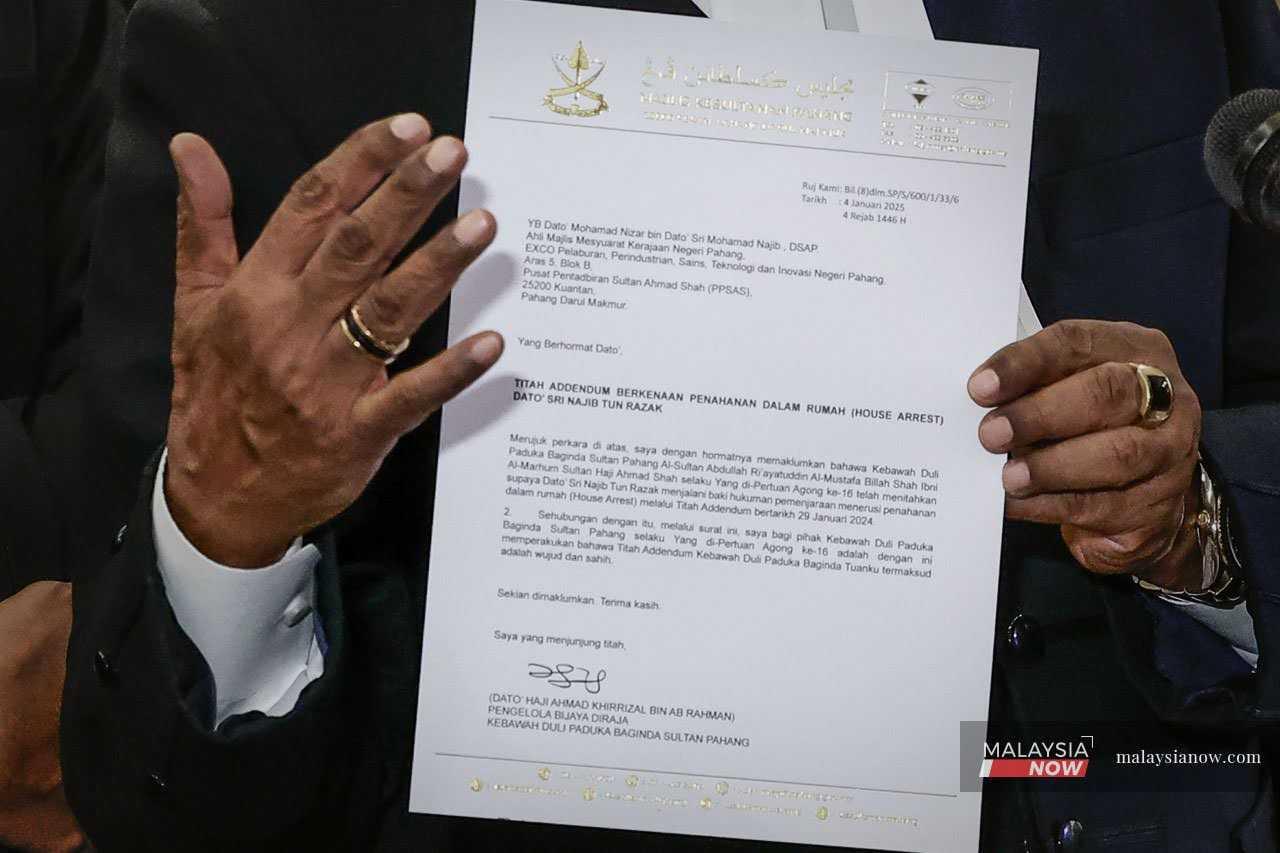

Just In

The Court of Appeal in Putrajaya today disallowed an application by lawyer Muhammad Shafee Abdullah, appearing for Najib Razak and his son Mohd Nazifuddin, to refer constitutional issues involving Section 106 (3) of the Income Tax Act 1967 to the Federal Court.

A three-member bench led by justice Abdul Karim Abdul Jalil decided to proceed with the appeal proper brought by the former prime minister and his son in connection with the Inland Revenue Board’s (LHDN) suit over the recovery of income tax arrears.

“We are not with you in respect of this application in bringing the matter to the Federal Court to determine the alleged constitutional issues of Section 106 (3),” Karim told Shafee.

The Court of Appeal judge said the court would prefer to proceed with the appeal proper which would cover the constitutional issues as well as other issues.

Karim, who presided with justices Vazeer Alam Mydin Meera and Supang Lian subsequently fixed Sept 9 to hear the appeals.

Shafee applied for an interim stay of the High Court order pending the appeal hearing but Karim said the court could not give an interim stay.

In today’s proceeding which was held online, Shafee sought for the Court of Appeal to refer five questions of law including the validity of Section 106 (3) as he said it was an important issue.

He said he would ask the Federal Court to sit on a quorum of five or seven to finally decide on the constitutional issues including a question on whether Section 106 (3) is unconstitutional and ultra vires as it usurps the judicial power of the court guaranteed by Article 121 of the Federal Constitution.

However, senior revenue counsel Hazlina Hussain disagreed, saying there was no ambiguity on the interpretation of Section 106 (3), adding that there was nothing unconstitutional in that section.

Section 106 (3) states that in any proceeding under this section, the court shall not entertain any plea that the amount of tax sought to be recovered is excessive, incorrectly assessed, under appeal or incorrectly increased.

Both Najib and Nazifuddin are appealing against the decisions of two separate High Courts which allowed LHDN’s applications to enter a summary judgment to recover tax arrears of RM1.69 billion from Najib and RM37.6 million from Nazifuddin, respectively.

On July 22, last year, High Court judge Ahmad Bache allowed LHDN’s application for a summary judgment to be entered against Najib in its suit to recover the RM1.69 billion in taxes from the latter for the period between 2011 and 2017.

Najib lost his bid in the High Court on June 14 this year to obtain a stay of execution on the summary judgment.

The board had on Feb 4 this year issued a bankruptcy notice against Najib following the Pekan MP’s failure to pay the amount, as the summary judgment was not stayed.

As for Nazifuddin, High Court judge Ahmad Zaidi Ibrahim on July 6 last year ordered him to pay RM37.6 million in unpaid taxes to LHDN after allowing its application to enter a summary judgment against him in its tax arrears suit seeking to recover the unpaid amount from him between 2011 and 2017.

He was served with a bankruptcy notice on April 30 over the failure to pay the amount.

A summary judgment is when the court decides a particular case summarily, without calling witnesses to testify in a trial.

Subscribe to our newsletter

To be updated with all the latest news and analyses daily.

Most Read

No articles found.